This AI-Fueled Stock Is Up 127% in 2025 But Still Looks Undervalued

/Western%20Digital%20Corp_%20logo%20on%20sign-by%20360b%20via%20Shutterstock.jpg)

The surge in artificial intelligence (AI) infrastructure spending has not only lifted the pure-play AI companies, but also those playing a crucial role in supporting its ecosystem. One of these such stocks is Western Digital (WDC), a company that manufactures data storage devices built on hard disk drive (HDD) technology.

So far this year, Western Digital’s shares have surged about 127%. The rally stems from solid demand for its data storage offerings. As AI adoption accelerates, the demand for massive storage capacity has exploded, with data centers and cloud providers securing high-capacity drives. This demand is running ahead of supply, driving prices higher and strengthening the bull case for companies like Western Digital.

Given the solid demand trends, Western Digital’s top line surged 51% in fiscal 2025. Further, its gross margin expanded significantly. Thanks to its solid revenue and earnings, the company is generating strong free cash flow, which is allowing it to deleverage its balance sheet.

What makes Western Digital stock even more compelling is that, despite its strong run-up, it still looks undervalued relative to its growth prospects. Does this mean the momentum in WDC stock is far from over? Let’s take a closer look.

AI-Led Demand Supporting WDC’s Growth

Looking ahead, the momentum in Western Digital’s business will likely sustain as demand for scalable, cost-efficient data storage will remain high. With large language models (LLMs) and the rapid adoption of agentic AI, generating, processing, and storing massive volumes of data, demand for HDD is set to increase. HDDs remain the go-to choice for high-capacity storage thanks to their reliability and lower cost per terabyte. This positions Western Digital well to benefit from hyperscale data centers and cloud providers racing to support AI-driven workloads.

The strong demand trends are reflected in its quarterly performance. Shipments of its latest generation ePMR drives, with up to 26 terabytes of storage, and UltraSMR drives, which reach 32 terabytes, more than doubled last quarter to 1.7 million units. These high-capacity drives deliver strong total cost of ownership benefits, which are driving adoption from hyperscale customers building out massive AI-ready data centers.

Looking ahead, Western Digital is preparing for another leap with its Heat-Assisted Magnetic Recording (HAMR) technology, which promises even greater storage density. Testing with hyperscale customers has been promising, with commercial rollout expected in 2027. Meanwhile, new ePMR drives will continue to fill the gap. This strategy ensures a smooth evolution of Western Digital’s technology roadmap while meeting customer demand.

The rapid growth of AI is also driving the company’s platform business. Its platform technology maximizes the performance and capacity of its drives. This side of the business is gaining traction with infrastructure providers and positions it well to capitalize on the demand from AI-native companies that do not have their own storage infrastructure teams.

The company continues to see strong momentum in Cloud, which represents a large and growing end market for its products. Notably, Cloud represented about 90% of its total revenue at the end of the fourth quarter of fiscal 2025.

Western Digital Stock Is Undervalued

Despite the stock’s sharp run-up, WDC’s valuations remain attractive given the company’s solid earnings growth outlook. Western Digital stock trades at a forward price-earnings ratio of just 16.22x. This appears cheap given the growth trajectory ahead. Analysts see WDC’s earnings per share climbing 32.89% in fiscal 2026, followed by another 13.29% jump in 2027, reflecting that the stock is undervalued.

The Bottom Line

Western Digital is a beneficiary of the AI-driven infrastructure boom, with surging demand for its high-capacity storage offerings. Its strong positioning in the HDD space, solid product portfolio, and innovations like HAMR position it well to capitalize on the AI-driven demand.

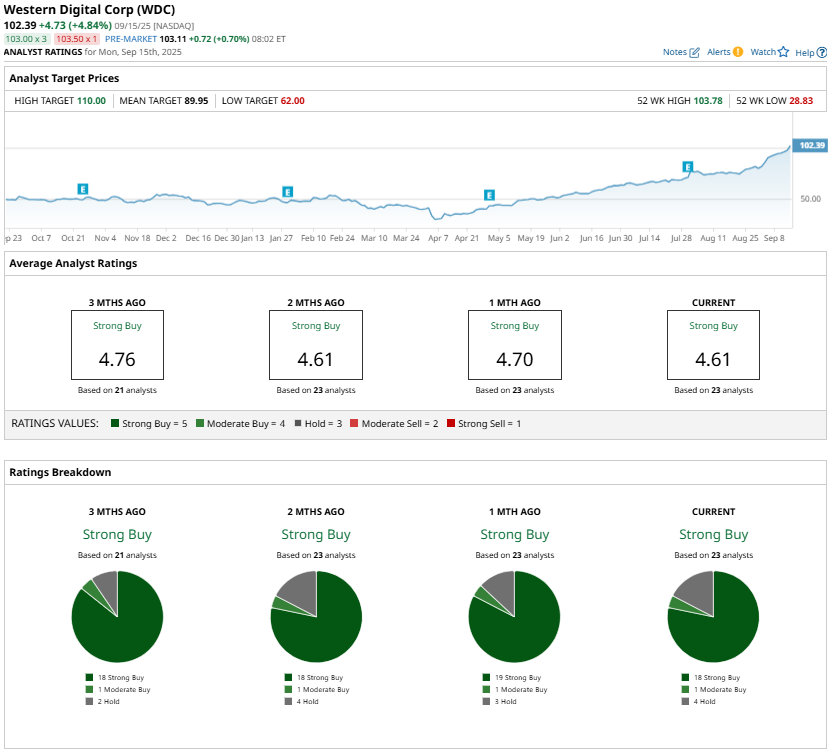

Even after a significant rally, the stock’s valuation remains compelling, suggesting further upside potential. Moreover, Wall Street is bullish about Western Digital stock and maintains a “Strong Buy” consensus rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.